Bitcoin looks set to finish Wednesday’s session broadly unchanged in the mid-$24,000, handing market participants some much-needed time to catch their breath after a hectic seven days of price action. This time last week, Bitcoin had just dropped back under $22,000 for the first time in over three weeks, weighed alongside downside in US stocks amid concerns about Fed tightening.

A string of high-profile US bank collapses (Silvergate, SVB and then Signature Bank) would trigger further risk-off flows, driving the BTC price as low as the $19,500s by Friday, where Bitcoin tested its 200DMA and Realized Price for the first time in nearly two months.

However, a proactive response from US authorities to backstop deposits and launch a new bank liquidity program (which helped USDC, a key part of the crypto market’s plumbing, recover back to its $1 peg) helped Bitcoin end last week on a strong footing.

Expectations that the risk of a banking crisis would deter the Fed from engaging in substantial further rate hikes, as well as narratives around cryptocurrencies like Bitcoin being a safe haven against trouble in the traditional financial system then helped propel Bitcoin as high as the mid-$26,500s by Tuesday.

That was Bitcoin’s highest level since last June and, at its peak this week, marked gains of over 35% versus last week’s sub-$20,000 lows. Bitcoin’s wild swing from two-month lows to nine-month highs in a matter of days has got traders betting that more volatility is likely now incoming. At least, that’s according to Bitcoin options markets. Let’s take a deeper look.

Traders Up Their Bitcoin Volatility Bets

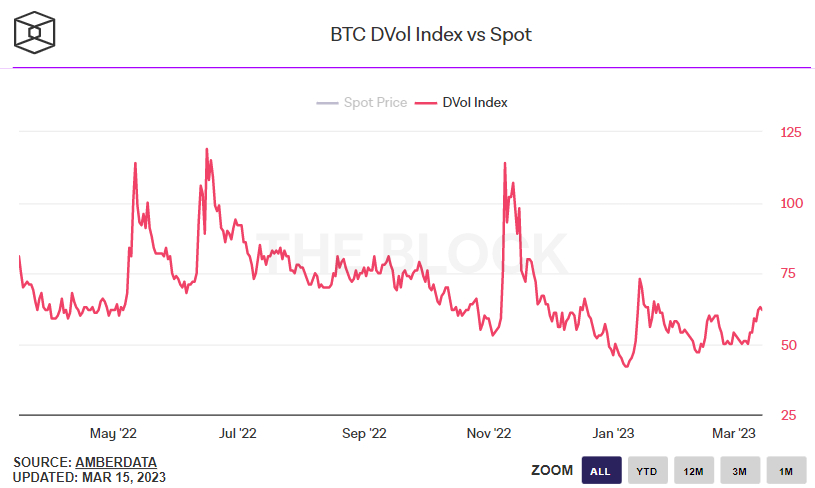

Over the course of the last week, Deribit’s Bitcoin Volatility Index (DVOL) has jumped from around 50 (which is not far above historic lows) to nearly hit two-month highs of around 62. That’s still below highs hit in January in the 73 area from when BTC burst back above $20,000. Deribit is the dominant crypto derivatives exchange.

And it’s still well below last year’s post-FTX collapse highs in the 114 area. But it still shows that investors are positioning for choppier waters ahead. And that makes sense when you consider the key $25,200-400 resistance area that Bitcoin breached this week, which technicians think opens the door to a potentially swift rally towards the next major resistance area around $28,000, and perhaps even above $30,000.

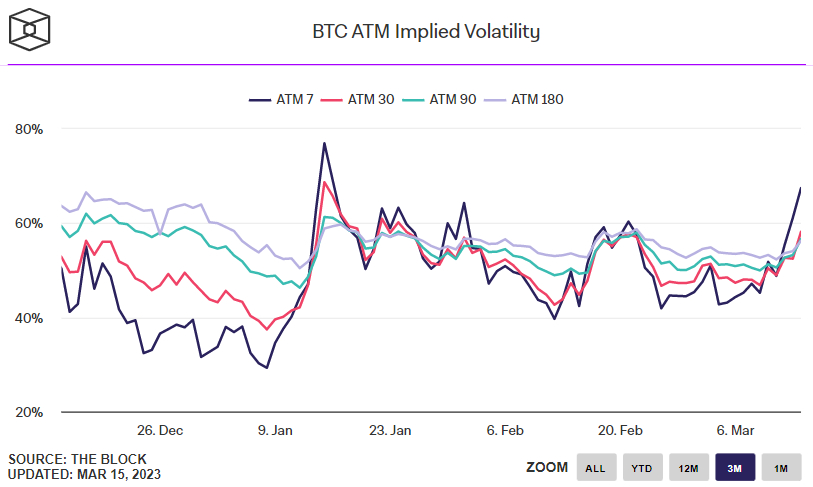

Meanwhile, implied volatility according to At-The-Money (ATM) Bitcoin option pricing has also been rising. ATM Implied Volatility of options expiring in 7-days hit its highest level since mid-January on Tuesday at 67.44%, up from earlier monthly lows in the 42% area. ATM Implied Volatility according to options expiring in 30, 90 and 180 days have all also risen to multi-week highs.

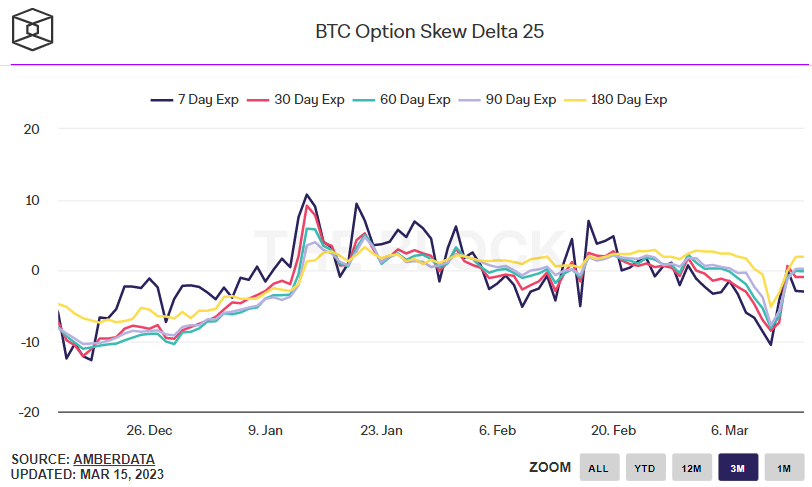

Traders Once Again Neutral on the BTC Price Outlook

When Bitcoin dipped under $20,000 for the first time in two months last week, the outlook for the BTC price according to the 25% delta skew of Bitcoin options expiring in 7, 30, 60, 90 and 180 days fell to their lowest levels of the year of between -5 to -10.

The 25% delta options skew is a popularly monitored proxy for the degree to which trading desks are over or undercharging for upside or downside protection via the put and call options they are selling to investors. Put options give an investor the right but not the obligation to sell an asset at a predetermined price, while a call option gives an investor the right but not the obligation to buy an asset at a predetermined price.

A 25% delta options skew above 0 suggests that desks are charging more for equivalent call options versus puts. This implies there is stronger demand for calls versus puts, which can be interpreted as a bullish sign as investors are more eager to secure protection against (or bet on) a rise in prices.

However, in wake of the recovery in the BTC price to nine-month highs, options markets have reverted to taking a broadly neutral view on the market. The 25% delta skew of Bitcoin options expiring in 7, 30, 60, 90 and 180 days are all back to close to 0.

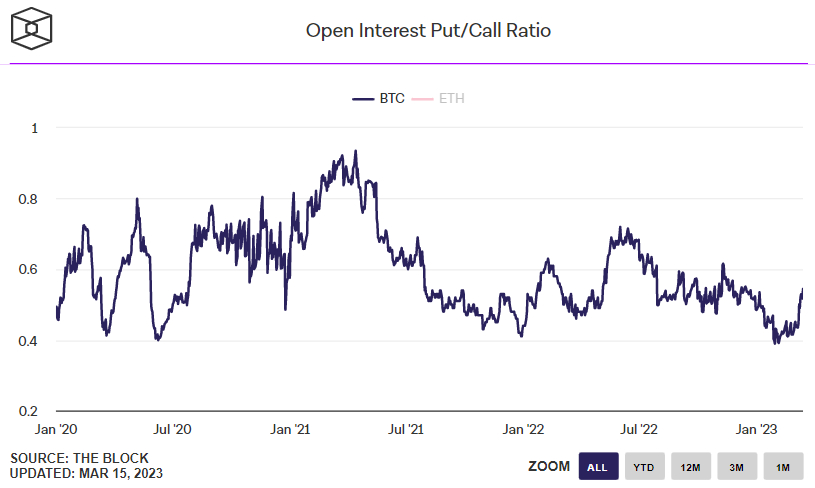

Sending a more bearish signal, however, is the ratio between Put and Call options on Deribit. The ratio between the open interest of Bitcoin put and call options was 0.54 on Wednesday, its highest level of the year and up from recent record lows under 0.40. A ratio below 1 means that investors favor owning call options (bets on the price rising) over put options (bets on the price dropping).

Credit: Source link

{kind=link}